HomeBUSINESSSanctions are working: Economic stats show their impact

Sanctions are working: Economic stats show their impact

Tyzhden: The war continues in Donbas, taking dozens of lives every day. The US and the EU have not abandoned their efforts to persuade Russia to stop promoting their terrorist proxies. Rumors of yet another round of sanctions are already floating in the West. In the meantime, while the Kremlin stubbornly continues its aggression, the Russian economy is loses the ground under its feet. A number of indicators show that US-European restrictions are having a negative impact on economic growth in Russia, even though Moscow denies this. And apparently, it will only get worse.

Most of todays’ data describing macroeconomic situation in Russia, is available up to the end of June, July, and up to early August. That covers the period when first and second rounds of sanctions against individuals and companies close to the Kremlin were in place. The impact on the economy of the third round, commenced with the actions that the United States launched in July 17, is barely reflected in available statistics, and thus will determine the deterioration of economic indicators in the III and IV quarters of this year and later.

Banks The most significant changes occurring in the economic relations of Russia with the external sector, are reflected in the balance of payments. For example, the local banks, which until recently could easily borrow abroad at a rate of LIBOR + 1% or less (by today’s standards it is less than 2% per annum, considering a 12 months period) and earned a lot of money on the interest rates difference, now hit the wall. The richest countries in the world (USA, Japan, EU members) refuse to further issue them credit. This is taking place in two ways. First, through direct prohibition to grant loans or assist in obtaining funds for more than 90 days to five largest Russian financial institutions (“Sberbank”, VEB, VTB, “Gazprombank” and Russian Agricultural Bank), which concentrate more than half of Russia’s banking assets. Second, by “verbal intervention”, i.e. persuading largest institutional and private investors of wealthy countries to avoid investments in Russia’s banking sector to avoid problems with the regulators and the like. And while in the first case, Russian banks can theoretically re-credit large amounts quarterly (but then they get hooked on a financial needle, which the West is able to withdraw almost instantly, causing their collapse), in the second case – global investors one by one turn their backs on Russia’ financial sector, looking for good investment opportunities elsewhere.

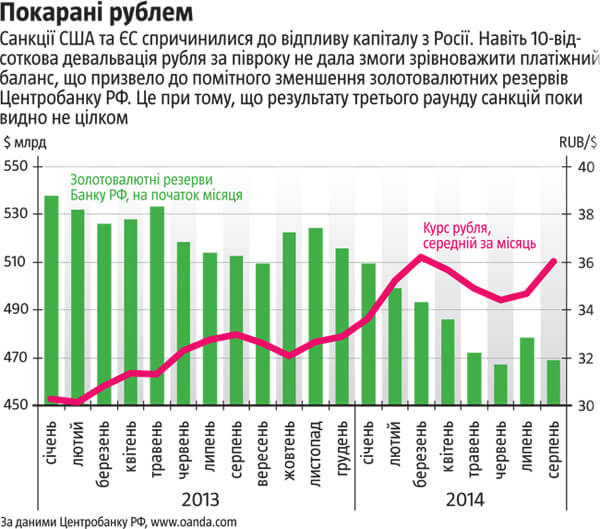

If the oil price decreases further, the overall impact on Russia’s budget can be daunting for Russia’s economy As a result, if Russian credit organizations obtained $ 5 -10 billion of net external financing quarterly in the past (direct investments, loans, bonds, etc.), in the 1Q of 2014, this amount was $0.9 billion, and fell in the 2Q to negative $10.9 billion (meaning that more money were returned than borrowed). Russian banks are forced to pay back money previously borrowed. To do this, they pump out capital from the economy of their country, leading to a chain of negative consequences.

The main result – is that financial institutions of Russia gradually lose their capacity to fund Kremlin’s geopolitical interests due to the lack of funds. Loans, like the one Putin granted to Yanukovych last year in December, as well as extensive network of banks in the countries under Moscow’s influence, through which agents of Russian special services are financed – these are some of the tools for implementation of Russia’s leader expansion projects. At present, they are losing their power, as statistics shows. In the second quarter of this year Russia’s money outflow volume to finance its assets abroad by its banks totaled $6.1 billion, which is 55% less than last year. Although it is still a large amount (in the first quarter it totaled $ 22.1 billion, but probably included the funds wired out of the country by many wealthy Russians, fearing a large-scale war or other aftereffects of Kremlin’s master). In recent years outflow of money from Russia in this category was $7-8 billion. Now, it will, apparently, decrease, which will eventually have a significant negative impact on Putin’s ambitions in the world.

Another consequence, this time internal, is the increased interest rates. Since Russian financial sector is now devoid of foreign investments at a former scale, funds in the domestic market become more scarce. Therefore, they become more expensive, which can be observed not only with the interest rates for short term operations on the interbank market, but also at the level of loans and deposits, the rates for which rose this year by 1-2 points. What is 1-2% for those who take a loan, looks like noting? Apparently not. Due to the increasing interest rates the volume of lending to individuals in Russia in the first half of 2014 was 4.2 trillion rubles. This is only 4.2% more than last year. At the same time, during the entire 2013 Russian banks issued loans to its citizens for 8.8 trillion rubles, which is 21.5% more than in the previous year. This means that in only six months the rate of growth in lending fell five times. This leads to a decreased Russian consumption. For example, in the first seven months of 2014 the market for new passenger cars in Russia has lost 10%, in July the rate of decrease was 23% (see. “No Money – No Car”), although this was partly due to the devaluation of the ruble (see. “Punished by the Ruble”). Retail trade turnover in July grew only by 1.1%, although in the past year added 3.9% in volumes.

The third consequence of the shortage of external financing for Russian banks – is loss of population’s trust. This will manifest in two aspects. First, the rate of deposit base growth decreases, even though population’s income is still growing. If in 2013 the funds on the bank accounts of individuals and legal entities added 14.2% in rubles and 11.5% in other currencies, in the six months of this year, it increased by 1.2% (to 26.8 trillion rubles) and 7.6% (9.8 trillion rubles) respectively. Increase of deposits in hard currency does not compensate for their low increase in rubles. Moreover, deposits of individuals in rubles even decreased by 2.2% (to 13.7 trillion rubles). Second, Russian citizens keep more and more savings in foreign currency under their mattress. If in previous years outflow of foreign cash currency from Russian banks was not major, in the range of $1 billion per quarter, and regularly changing into inflow, in the first half of 2014 the cash outflow totaled $12.1 billion. For Russia it is a big deal, since, unlike Ukraine, Russians have long been measuring all the prices in rubles (expensive goods, cars, real estate) due to the relative stability of the latter, until recently. And a cash outflow of such scale this year indicates deepening distrust of Russians to their banking sector and national currency. This is a first sign of slide-down of local banks to the level of, say, Ukrainian banks (with low-quality balance sheets and regular crises) and the first signs of a general public distrust of government in general.

Russian bankers don’t have reasons to panic yet. But negative trends, generated or enhanced by the sanctions against Russia, are very stable and can last a while. If so, Russia’s banking sector will shortly not only be unable to finance geopolitical stunts of the Kremlin, but also will fall to the level of many chronically insolvent banks. Even now Russia is forced to take the unprecedented step: recently Ministry of Finance announced the plans to spend 239 billion rubles of the National Welfare Fund (NWF) to purchase shares of VTB and “Russian Agricultural Bank”, which fell under direct sanctions, in order to recapitalize them. If the second and sixth highest rated banks already need public investments for recapitalization, what will the scale of the problem be and how will it increase when the third round of sanctions brings its full effects and lasts for at least a year?

Companies The situation with the Russian business is very similar. This is especially true for large companies who regularly obtain foreign funding. Russian entrepreneurs used to attract external funding of $10-15 billion quarterly. The great share of that amount came as a foreign direct investment (FDI), which together with the new technologies and management methodologies formed grounds for economic growth in Russia. At the moment these volumes are significantly lower. In the first quarter of 2014, Russian companies attracted $8.4 billion net foreign financing (FDI reached $9.8 billion) in the second – only $4.3 billion ($7.3 billion, respectively), which is 58% less than last year. Many non-residents freeze their investment projects in Russia by cutting their funding. And this applies not only to quasi-governmental institutions, like EBRD, which to some extent are dependent on the policy. With the pause of foreign investment, Russia’s economy loses not only limited portions of imported technologies that allowed it to move forward somehow. It will have no real growth factor. Statistics confirm this: gross capital formation (investment) in the first quarter in real terms has lost 15%, fixed capital – 7%. In the second, perhaps, only worse investment dynamics can be expected. And, as we know from the theory, investment decrease is the direct reason of employment and economic regression.

External debts of Russian corporations are also in trouble. They had traditionally borrowed at global markets, as they had open access. In recent years, in the era of cheap money, they could afford long term loans at 2-5%. Deprivation of Russians of their ability to borrow abroad will cost them dearly. The same loans in foreign currency in Russia will now cost 6-8% and 9-12% in rubles. What does this mean? When you imagine that at least 1/3 of Russia’s gross external debt, which as of mid-2014 totaled $721 billion, will have to be financed from the domestic market (about as much as local companies owe non-residents – $269 billion), this will increase financial costs of Russian business by $10.8 billion, in case of refinancing in foreign currency, or $18.8 billion if the new internal loans will be provides in rubles (387 billion rubles and 678 billion rubles respectively). Since in the first half of 2014 the net income of business in Russia was about 3.6 trillion rubles, with the increased cost the profit of its companies will fall by 5-9%. And domestic financial sector still has to find these funds somewhere, which will cause a further rise in interest rates and a serious costs to Russian entrepreneurs.

Ultimately, such developments promises numerous bankruptcies, let alone the significant drop in the real value of assets, operating in Russia. In less than one to two years the consequences of US-European sanctions will be fully noticeable. For now we see only their earliest manifestation. For example, in early March for 10 days after the first round of sanctions’ was announced, Russian shares (RTS index) fell by 14.9%, while the market lost more than $60 billion capitalization. Following the announcement by the United States of the third round of sanctions and Malaysian aircraft crash in two weeks securities lost 14%. For now the Russian market is able to recover after such steep falls, but with the growth and accumulation of negative effects of the constraints, the wealth of Russian oligarchs and Kremlin leaders will melt significantly. As to the financing of Russian business, Russian Federation is trying to somehow replace it with domestic resources. That is why bankers have limited consumer loans, while bank financing for business is growing faster. Thus, in the first half of the year Russian financial institutions issued them 15.3 trillion rubles in loans, which is 11% more than last year. However, this is not enough, because for a full replacement of external borrowing companies of Russia should further find almost 10 trillion rubles in the domestic market. In the current situation it is a tough task. And it is still unclear what rates will these resources have and whether it will turn Russian business into constantly unprofitable.

One way or another, but the United States and the EU sanctions against Russia are working. According to Russia’s Central Bank, the net capital outflow in the first half of 2014 reached $75 billion, almost twice as much as last year. This happened before the third round of restrictions and has already led to a significant devaluation of the ruble and reduced golden reserves of Russian regulator (see. “Punished by the Ruble”). With the introduction of the new sanctions Moscow will be loosing money at a much faster pace, so the forecasts of Russian economists, according to which the total capital outflow in 2014 will be $150-200 billion, may, ultimately, prove to be optimistic. Russia’s economy has a good chance to enter a recession this year. Even Russia’s Economic Development Minister Alexei Ulyukayev recognizes this. Although he says that not the “geopolitical change” (read: sanctions), but poor quality of market institutions is the main reason. However, if not for external interventions, the economy of Russia could have been in stagnation for few more years, showing zero growth rate. Then Putin and company would not even think about stealing less money and transferring them abroad. Instead, now we see the opposite picture. The amount of suspicious transactions (fake sale/purchase of goods and securities in order to transfer money to the offshore) in the first half of 2014 totaled $3.6 billion, which is 4.8 times less than last year. Thats how Putin forces Russian millionaires to give up the transfer of their capital abroad in the situation of deteriorating balance of payments under the influence of sanctions!

But even these amounts – nothing compared to the impact of the dropped energy prices. For the last two months oil (WTI – Russian analogue) fell by almost 10%, to $94 per barrel. Regardless of whether this is a regular fall, the impact on the balance of payments of the Russian Federation is the largest of all. Last year energy exports from there was $350 billion. If the price stays at the decreased level, Russia will lose one tenth of that amount – $35 billion. This is almost half of the volume of capital outflow, which took place in the first half of the year. If the price of oil will go further down, the overall effect on the balance of payments and the federal budget can be daunting for the economy of Russia. Then, quite possible, Putin might regret touching Ukraine. But it may be too late.

WE NEED YOUR HELP! 24/7, every day, since 2014 our team based in Kyiv is bringing crucial information to the world about Ukraine. Please support truly independent wartime Pulitzer Prize-winning journalism in #Ukraine.